RetirementPlan is a crucial step towards securing your financial future. When looking at crafting a comprehensive retirement plan, one potential tool that often comes up is annuity income. Annuities offer a steady stream of income during retirement, providing a layer of security. However, they also come with their own set of complexities and considerations. Understanding how annuities fit into your overall retirement strategy is necessary for making informed decisions and ensuring a stable financial future.

Key Takeaways:

- Annuity income can provide a steady stream of income during retirement: Annuities offer a way to receive regular payments for a specific period or for the rest of your life, helping you maintain financial stability in retirement.

- Helps in covering important expenses: Annuity income can be used to cover important expenses such as housing, healthcare, and daily living costs, ensuring you have a reliable source of income even when other retirement savings may fluctuate.

- Offers protection against outliving savings: Annuities can serve as a safeguard against outliving your savings by providing guaranteed income, offering peace of mind and financial security in retirement.

The Importance of Income in Retirement

The key to a successful retirement plan is ensuring a steady stream of income that will support you throughout your golden years. Without a reliable source of income, retirees may find themselves struggling to cover important expenses, leading to financial stress and uncertainty. This is where annuity income can play a crucial role in providing a consistent and predictable cash flow in retirement.

Ensuring a Steady Stream of Income

With the unpredictability of market fluctuations and the risk of outliving your savings, having a source of guaranteed income like an annuity can offer peace of mind and financial security. An annuity can provide a steady stream of income for life or a set period, helping retirees maintain their standard of living and cover ongoing expenses without worrying about market volatility.

Avoiding Financial Stress in Retirement

On the flip side, retirees who rely solely on investments subject to market risks may experience financial stress when faced with economic downturns or unexpected expenses. This can lead to having to withdraw more from their savings, potentially depleting their nest egg quicker than planned. However, incorporating annuity income into a retirement plan can help mitigate this risk by ensuring a portion of income is guaranteed, no matter the market conditions or how long you live.

This diversification in income sources can protect retirees from the negative impacts of market fluctuations and provide a sense of financial stability in retirement. It’s important to consider all options and work with a financial advisor to determine the best mix of income sources to support your retirement lifestyle.

Annuity Income as a Retirement Solution

What is Annuity Income?

Income annuities are financial products designed to provide a steady income stream during retirement. Essentially, when you purchase an annuity, you are entering into a contract with an insurance company. In exchange for a lump sum payment, the insurance company guarantees to pay you a regular income for a specific period or the rest of your life. Annuities can be a reliable source of income in retirement, helping to supplement other retirement savings and Social Security benefits.

How Annuity Income Works

To start receiving annuity income, you typically make a lump-sum payment to the insurance company. The amount of income you receive depends on various factors, such as your age, the size of your initial investment, the type of annuity, and prevailing interest rates. Annuities can offer fixed, variable, or indexed returns based on how the underlying investments perform.

This type of retirement income vehicle can provide a sense of security for individuals concerned about outliving their savings. Annuities can also help protect against market volatility, as some types offer guaranteed payouts regardless of market conditions.

Types of Annuities: Fixed, Variable, and Indexed

- Fixed Annuities: Offer a guaranteed interest rate for a specified period, providing predictable income.

- Variable Annuities: Allow you to invest in a selection of sub-accounts, offering the potential for higher returns but also subject to market risk.

- Indexed Annuities: Tie returns to a market index, offering the opportunity for growth while providing a level of downside protection.

After weighing the pros and cons of each type of annuity, individuals can choose the one that best aligns with their retirement goals and risk tolerance.

Benefits of Annuity Income in Retirement

Not sure what an annuity is and how it fits into your retirement planning? Check out What is an annuity? | Retirement Planning for more information.

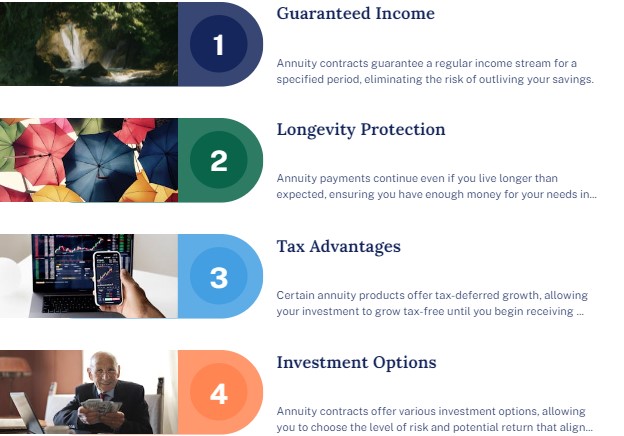

Guaranteed Income for Life

Benefits: An annuity provides a guaranteed income stream for life, offering stability and predictability in retirement. This can alleviate concerns about outliving your savings or market fluctuations affecting your income. With an annuity, you can enjoy peace of mind knowing you have a reliable source of income no matter how long you live.

Inflation Protection

Income: An important benefit of annuities is their potential to provide inflation protection. Some annuities offer riders or options that allow your income to increase over time, helping you maintain your purchasing power as prices rise. This can be crucial in ensuring your financial security throughout retirement.

This inflation protection feature can help safeguard your standard of living as you age, keeping pace with increasing costs for healthcare, living expenses, and leisure activities.

Tax Benefits

Guaranteed: One of the major advantages of annuities is their tax-deferred growth potential. When you invest in an annuity, your earnings grow tax-deferred until you start receiving payouts. This can help your money grow faster compared to taxable investments, allowing you to potentially accumulate more for retirement.

Benefits: Additionally, annuities offer the advantage of tax-efficient distributions. Depending on the type of annuity and how you structure your withdrawals, you may have the opportunity to spread out the tax impact over time, potentially reducing your tax liability in retirement.

How Annuity Income Fits into a Comprehensive Retirement Plan

Many individuals are turning to annuities as a key component of their comprehensive retirement plans. An annuity can provide a steady stream of income during retirement, offering financial security and peace of mind. When incorporated thoughtfully into a retirement strategy, annuities can serve several important purposes.

Diversifying Your Income Streams

Into diversifying your income streams is a crucial aspect of retirement planning. By adding an annuity to your portfolio, you can create a reliable source of income that is not tied to the fluctuations of the stock market. This can help protect you against market volatility and ensure that you have a steady stream of income regardless of economic conditions.

Reducing Reliance on Other Assets

Any reduction of reliance on other assets is imperative for a secure retirement. By using an annuity to supplement your other sources of income, you can reduce the risk of outliving your savings. An annuity provides a guaranteed income stream that you can depend on for the rest of your life, helping to alleviate the pressure on your other retirement assets.

It is crucial to consider the role annuities can play in spreading out your risk and ensuring a more stable financial future. By diversifying your income streams and reducing reliance on other assets, you can create a well-rounded retirement plan that is designed to last a lifetime.

Creating a Sustainable Retirement Income Strategy

Strategy, annuities can be a valuable tool in creating a sustainable retirement income strategy. By incorporating an annuity into your overall plan, you can ensure that you have a reliable source of income that will continue throughout your retirement years. An annuity can provide a consistent stream of income that can cover imperative expenses, allowing you to enjoy your retirement without worrying about financial stress.

Plus, annuities offer options for customization, allowing you to tailor your annuity to meet your specific financial goals and needs. Whether you are looking for guaranteed income for life or protection against market downturns, there is an annuity product that can align with your retirement objectives. By working with a financial advisor, you can determine the best way to incorporate annuities into your comprehensive retirement plan for a more secure financial future.

Common Misconceptions About Annuity Income

Your retirement plan may benefit from incorporating annuity income, despite some common misconceptions surrounding this financial tool. According to THE ROLE OF ANNUITIES IN YOUR RETIREMENT … report, there are various concerns about complexity, cost, and estate planning that can influence individuals’ perceptions of annuities.

Addressing Concerns about Complexity

On the surface, annuities may seem complex due to the different types and features available. However, with the guidance of a financial advisor, you can navigate these complexities and tailor an annuity that aligns with your retirement goals and risk tolerance. Understanding the terms and benefits of annuities can help you make informed decisions and feel confident about your financial future.

Debunking Myths about Cost

Cost is a common misconception when it comes to annuities. Some believe that annuities come with high fees that erode potential returns. However, modern annuity products offer a variety of fee structures, including options with low fees. It is crucial to carefully review the terms of an annuity contract and compare fees across different products to find one that suits your financial needs.

Clarifying the Role of Annuities in Estate Planning

One of the misconceptions about annuities is their perceived impact on estate planning. Some individuals believe that annuities may complicate the distribution of assets to heirs. However, annuities can be structured in a way that supports your estate planning goals, such as providing a steady income stream for a surviving spouse or beneficiaries. For instance, a joint-life annuity can ensure that both you and your spouse receive income for life, offering financial security to your loved ones.

Evaluating Annuity Income Options

Despite the mixed opinions on annuities, they can play a crucial role in a comprehensive retirement plan. According to Annuities: An important slice of the retirement pie, annuities offer a way to secure a steady income stream in retirement, which can be important for those looking to supplement their Social Security benefits and other retirement savings.

Assessing Your Retirement Goals and Needs

On your journey to evaluate the role of annuities in your retirement plan, it’s important to first assess your retirement goals and needs. Consider factors such as your desired lifestyle in retirement, expected expenses, and how much guaranteed income you will need to cover importants like housing, healthcare, and daily living expenses.

Comparing Annuity Products and Providers

| Annuity Products | Annuity Providers |

| Fixed Annuities | Insurance Companies |

| Variable Annuities | Financial Institutions |

Annuities come in various forms, each with its own features and benefits. It’s important to compare different types of annuity products and providers to find the best fit for your financial goals and risk tolerance. Consider factors such as fees, investment options, and the financial strength of the provider before making a decision.

Considering Fees and Charges

When evaluating annuity options, it’s crucial to consider the fees and charges associated with each product. Comparing these costs across different products can help you assess the overall impact on your returns. Some annuities may come with high fees that can eat into your earnings over time, so it’s important to weigh the fees against the benefits offered by the annuity.

This comprehensive evaluation will help you make an informed decision about incorporating annuity income into your retirement plan, ensuring that it aligns with your financial goals and provides a reliable income stream in your golden years.

Final Words

The role of annuity income in a comprehensive retirement plan cannot be understated. Annuities can provide a guaranteed income stream during retirement, which helps to alleviate the risk of outliving your savings. This steady income can offer peace of mind and financial security, allowing you to enjoy your retirement years without constantly worrying about market volatility or economic downturns.

The key is to carefully consider your financial goals and needs before deciding if annuities are the right option for you. By incorporating annuity income into your retirement plan, you can create a well-rounded strategy that combines various sources of income to support your desired lifestyle in retirement. Keep in mind, diversification is key, and consulting with a financial advisor can help you make informed decisions that align with your long-term financial objectives.

FAQ

Q: What is annuity income and how does it work in a retirement plan?

A: An annuity is a financial product sold by insurance companies designed to provide a stream of income in retirement. It works by investing a lump sum of money in exchange for guaranteed periodic payments, typically for the rest of your life.

Q: What role does annuity income play in a comprehensive retirement plan?

A: Annuity income can play a crucial role in a comprehensive retirement plan by providing a guaranteed source of income that you cannot outlive. It can help cover necessary expenses, reduce the risk of running out of money in retirement, and provide peace of mind.

Q: What are the types of annuities available for retirement planning?

A: There are several types of annuities available for retirement planning, including immediate annuities, deferred annuities, fixed annuities, variable annuities, and indexed annuities. Each type offers different features and benefits, so it’s necessary to choose one that aligns with your financial goals.

Q: Are there any drawbacks to including annuities in a retirement plan?

A: While annuities can provide a secure source of income in retirement, they also come with drawbacks. These can include high fees, limited access to your money, complex terms and conditions, and potential tax implications. It’s necessary to weigh the pros and cons before including annuities in your retirement plan.

Q: How can I determine if annuity income is right for my retirement plan?

A: To determine if annuity income is right for your retirement plan, consider factors such as your risk tolerance, financial goals, time horizon, and overall financial situation. Consulting with a financial advisor can help you evaluate whether annuities align with your retirement objectives and create a comprehensive plan tailored to your needs.